Margin Estimate | AlgoTest

It's crucial to understand the required margin for executing a strategy. If your margin is insufficient, your broker may reject your orders, effectively stopping your strategy. This could result in missing out on a profitable opportunity if the day turns in your favour. Therefore, it's essential to know the margin requirements in advance before putting a strategy into action.

AlgoTest's Estimate Margin feature allows you to proactively check the required margin for your trading strategy. With this tool, you can confidently proceed with your strategy without any worries about meeting margin requirements. This ensures a smooth and seamless execution of your trading plan.

How to Use AlgoTest's Estimate Margin feature

To utilise the AlgoTest Estimate Margin feature, please follow the steps outlined below:

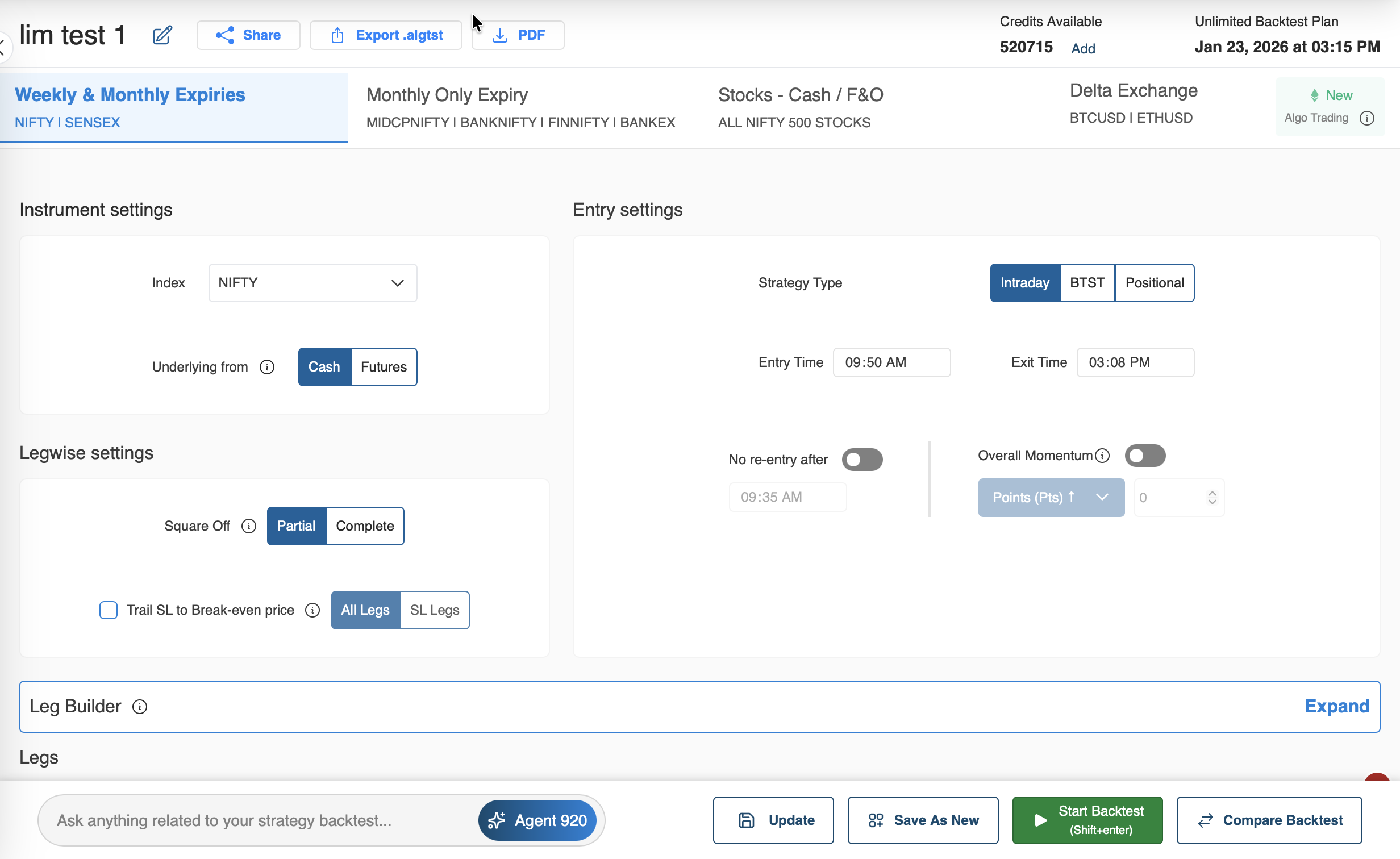

- Start by creating and backtesting the strategy for which you want to understand margin requirements. Click the "Start Backtest" button to begin.

- To proceed, scroll down and click on the "Calculate Margin" button depicted in the image below.

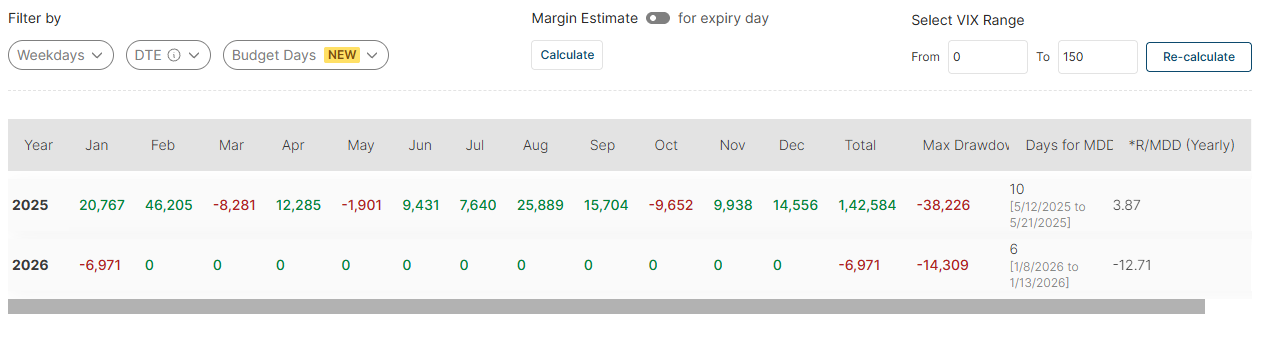

- It will display the margin required to execute the strategy depicted in the image below.

NSE F&O Margin – Short Summary

Margin is the amount required to take a Futures & Options position and is risk-based, not based on contract value.

Margin Components

-

SPAN Margin: Calculated by NSE using worst-case risk scenarios (price, volatility, time). Changes daily.

-

Exposure Margin: Additional safety margin charged by NSE/brokers.

-

Option Premium: Option buyers pay only the premium (no SPAN/exposure).

Margin Calculation

-

Futures:

SPAN + Exposure -

Option Selling:

SPAN + Exposure – Hedge Benefit (if any) -

Option Buying:

Option Premium only

Hedged positions require significantly lower margin than naked positions.

How SPAN Margin Is Calculated

SPAN is a risk-based margin representing the maximum possible loss under predefined NSE market scenarios.

NSE evaluates each position across multiple scenarios involving:

-

Price movement

-

Volatility changes

-

Time decay

For every scenario, NSE calculates the potential profit or loss.

The highest loss among all scenarios becomes the SPAN margin.

SPAN = Maximum loss across all risk scenarios

Hedging caps maximum loss, which reduces SPAN margin accordingly.

Key Points

-

Margin changes daily due to price, volatility, and expiry.

-

Exact SPAN values cannot be calculated manually (proprietary NSE model).

-

Always keep a buffer, as brokers may add extra margin.

To summarize:

SPAN margin = Maximum potential loss of a position under NSE’s worst-case market scenarios.

Please note:

-

The margin displayed is an approximate margin provided by NSE. Brokers may charge additional fees, so it's advisable to add a buffer to it.

-

Currently, you can view the margin required for a specific strategy. Information for the entire portfolio will be available soon.