Backtesting

Backtesting runs your complete strategy - signals plus the trade they execute against historical market data, so you can evaluate performance before risking anything.

Indicator strategy backtesting is included in the 6 Month Signal Plan. See Pricing & Plans.

Signals say when - a trade says what

Your signal defines when to enter and exit. To backtest, you must also define what gets traded when the signal fires: which legs (options/futures), how many lots, and any risk settings. This trade definition uses AlgoTest's standard Strategy Builder (the same one used for time-based strategies - you may see it referred to as a "920 strategy" elsewhere; it's just a trade configuration).

The 920/AlgoTrade page itself is for time-based strategies. For signal strategies, you only use the Strategy Builder to define the trade - you never need to activate anything from the 920 page. See the FAQ.

Run a backtest

-

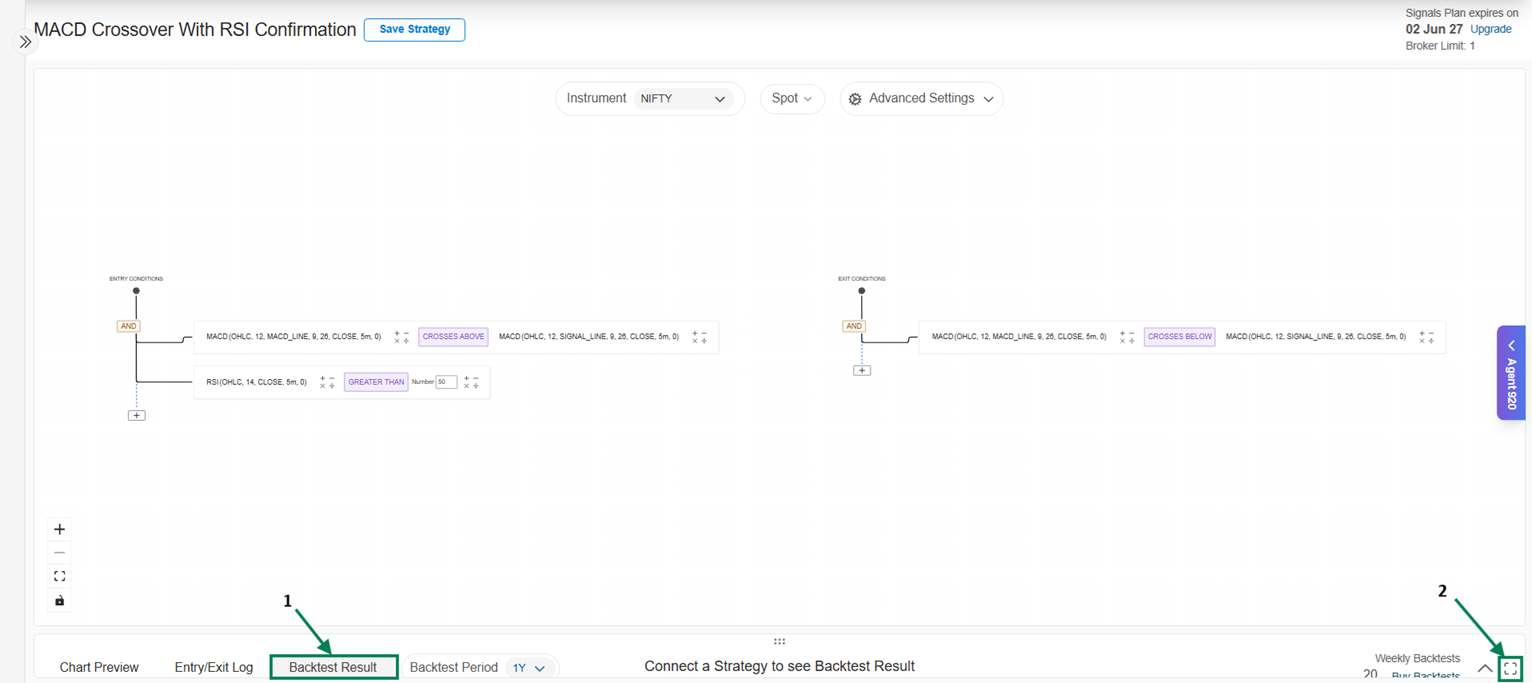

On your signal, click Backtest Result (use Maximize for full screen).

-

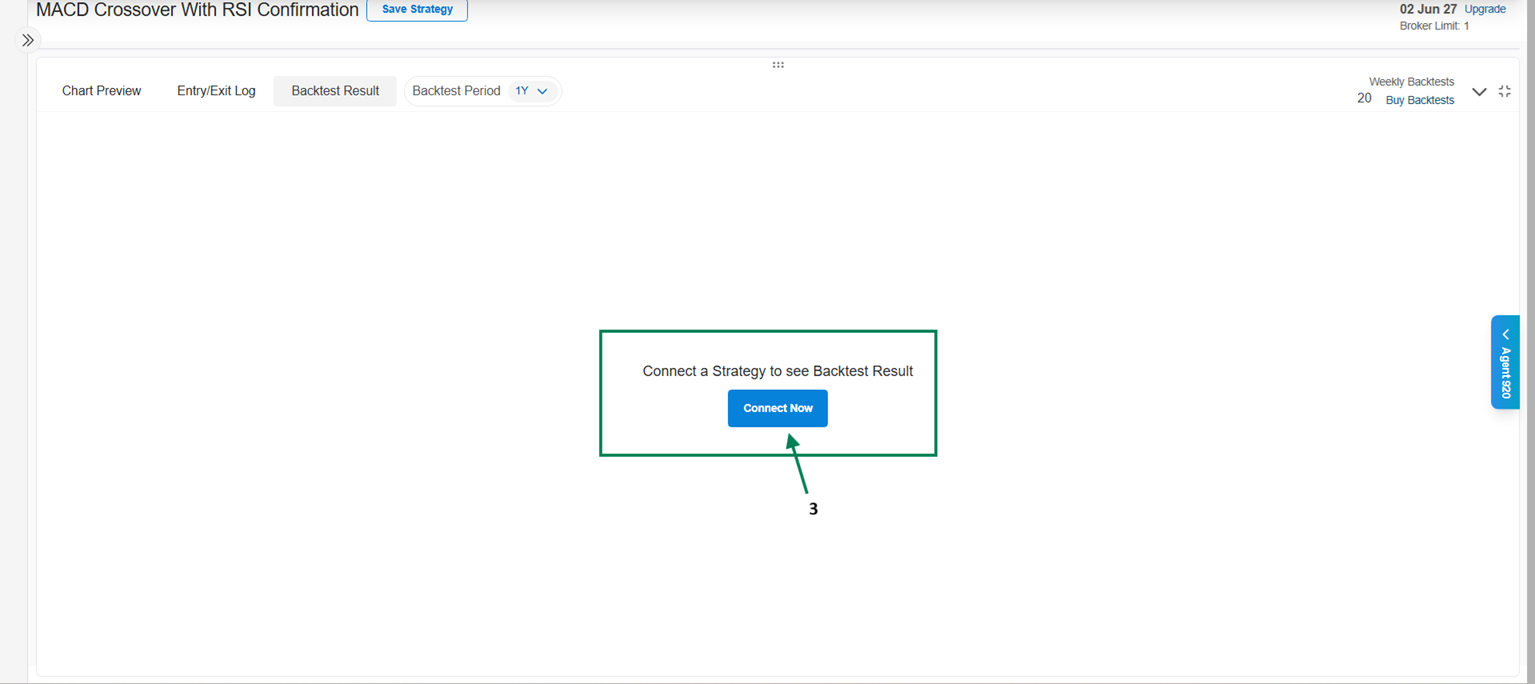

Click Connect Now, then either pick an existing strategy from your account or click Create Strategy.

-

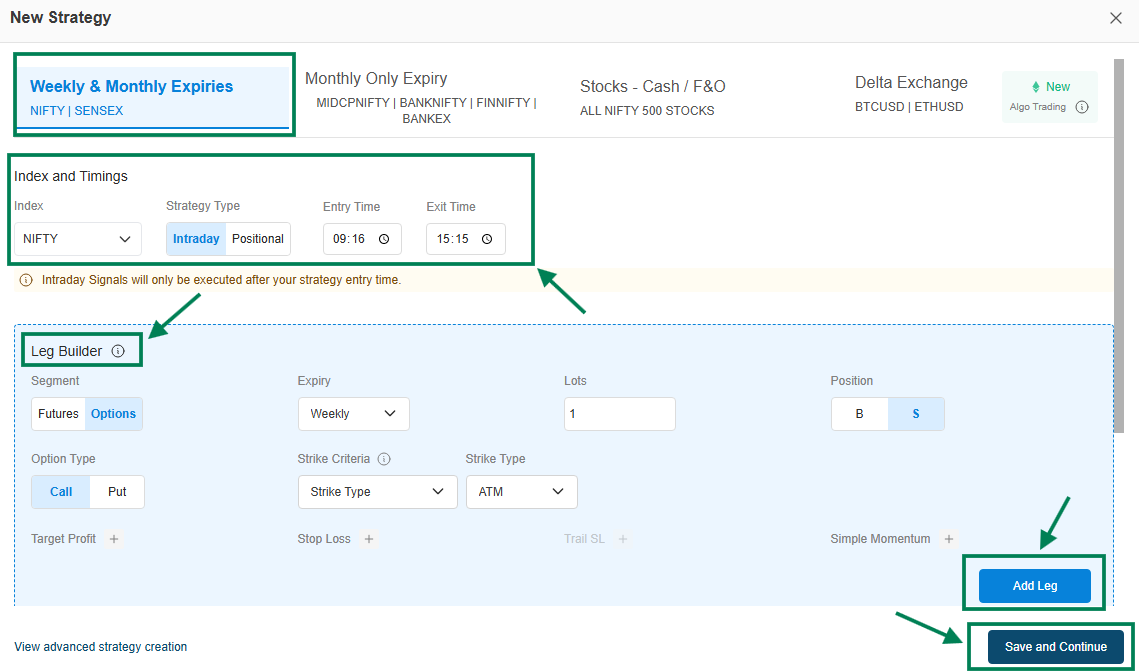

If creating new, configure the trade in the Strategy Builder:

- Index and Timings — index

- Leg Builder — segment, expiry, lots, position (buy/sell), option type, strike criteria; click Add Leg for each leg

- Optional risk settings — Target Profit, Stop Loss, Simple Momentum, and overall-strategy settings (Overall SL/Target, Lock Profit, Trail SL)

Click Save and Continue.

-

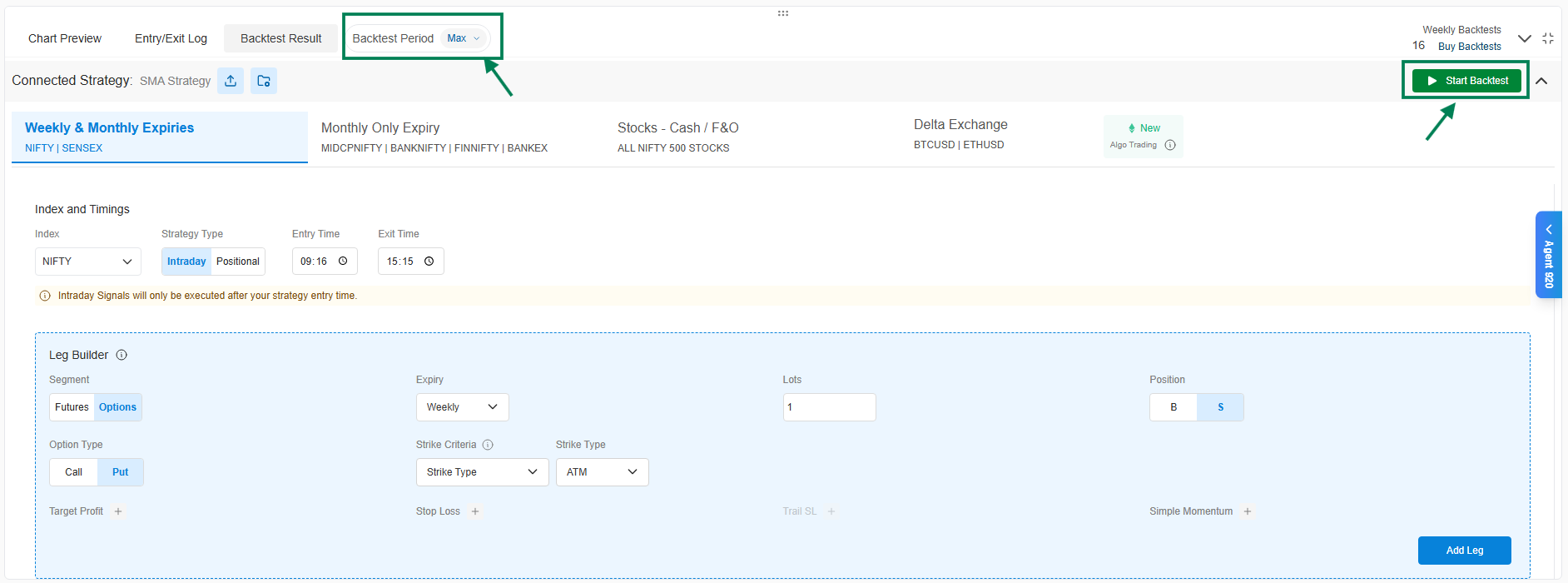

Select the Backtest Period and click BackTest.

Reading the results

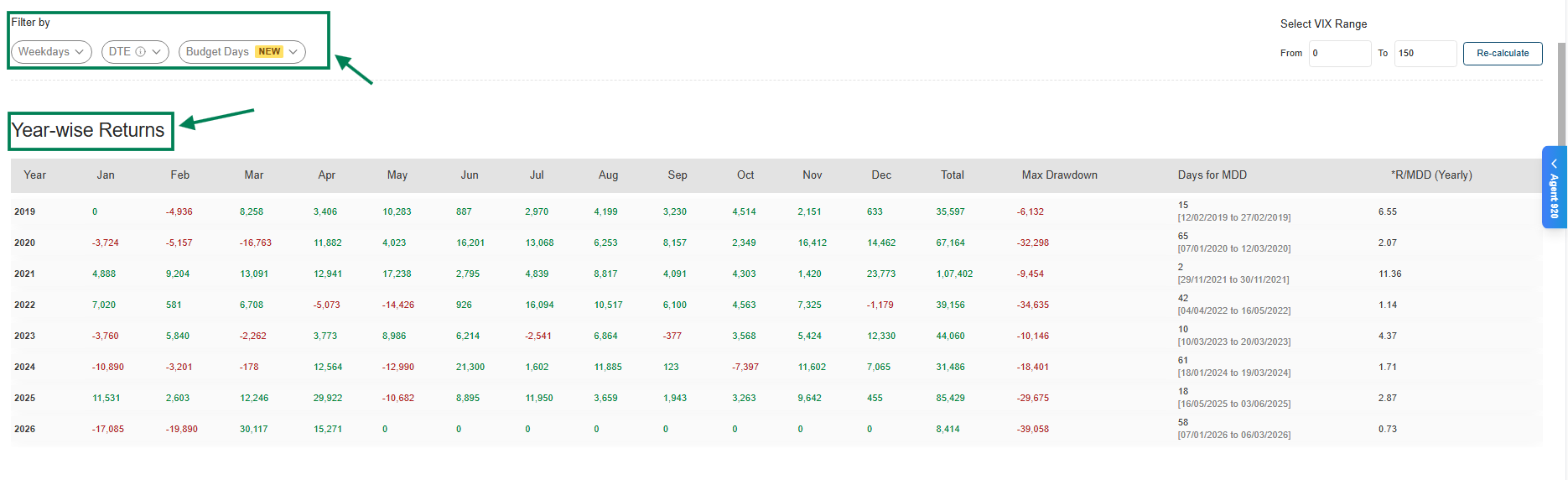

Year-wise Returns - performance per year: consistency check across different market regimes.

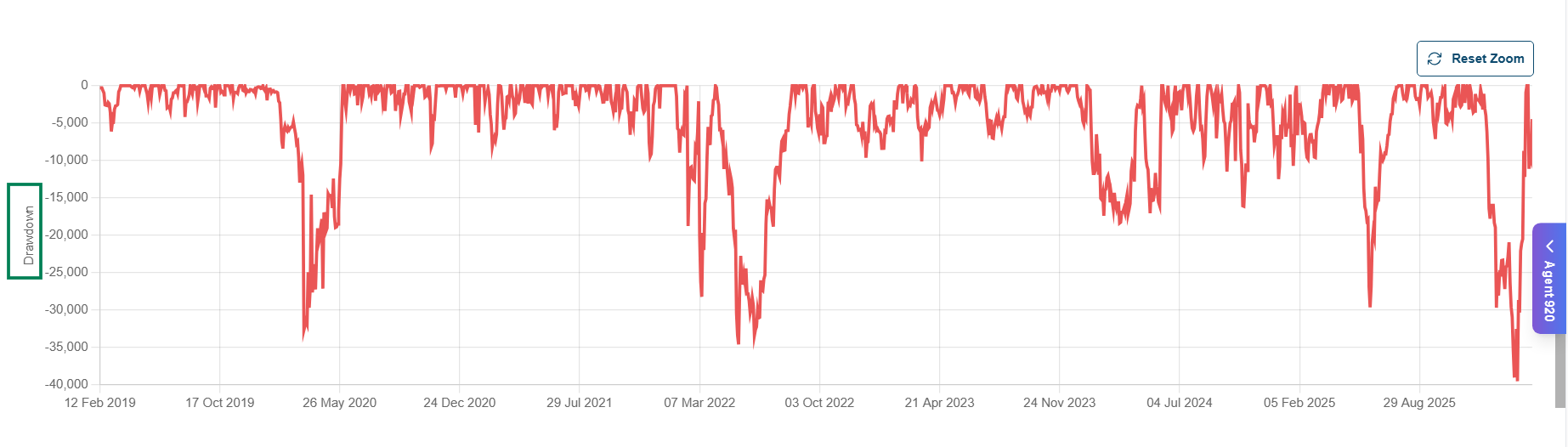

Max Drawdown - the largest peak to trough decline: the worst losing stretch you'd have sat through.

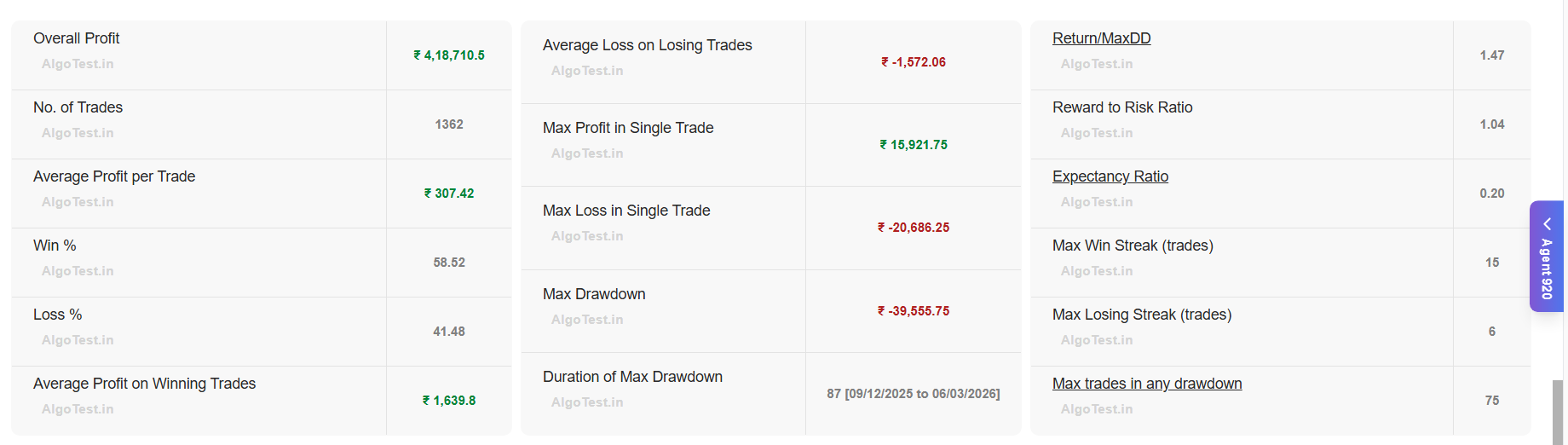

Strategy Stats - total P&L, number of trades, win rate, average profit/loss, risk-reward ratio, and winning/losing streaks.

Full Report - daywise trade logs, downloadable as CSV, sortable by P&L or day.

What to look for

| Metric | Question it answers |

|---|---|

| Win rate + avg win/loss | Does the edge come from many small wins or few large ones? |

| Max drawdown | Could you psychologically and financially survive the worst stretch? |

| Year-wise returns | Does it work across market regimes, or only in one lucky year? |

| Number of trades | Enough trades to be statistically meaningful (not 5)? |

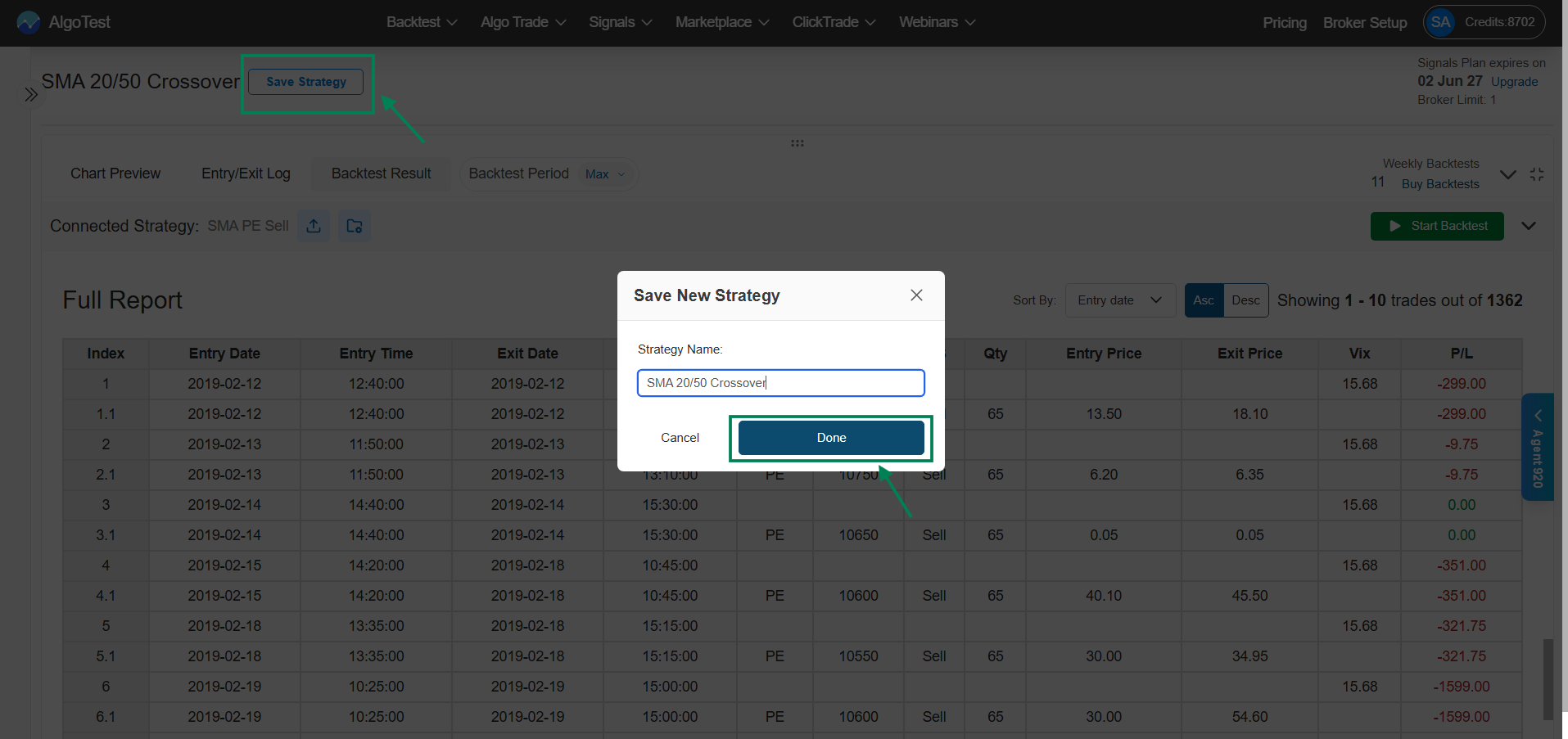

Save the strategy

Satisfied? Click Save Strategy, name it, and save. It will appear in Saved Signals, ready to deploy.

Backtests don't capture slippage, order fills, and execution latency the way live markets do. Always forward test before going live. See why results can differ.