Understanding Option Chain

Introduction to Option Chain and AlgoTest's Simulator

Understanding option chains is crucial for traders who want to make well-informed decisions in the options market. An option chain displays all available option contracts for a specific underlying asset, providing details such as strike prices, expiration dates, last traded price (LTP), and important metrics like delta and IV (implied volatility).

AlgoTest's new Simulator feature helps users analyse and test their trading strategies using historical option chain data. This allows traders to simulate past market conditions, assess the performance of their strategy, and make adjustments before implementing them in live trading. Ultimately, it helps traders refine and optimise their options trading approach.

Overview of Option Chain

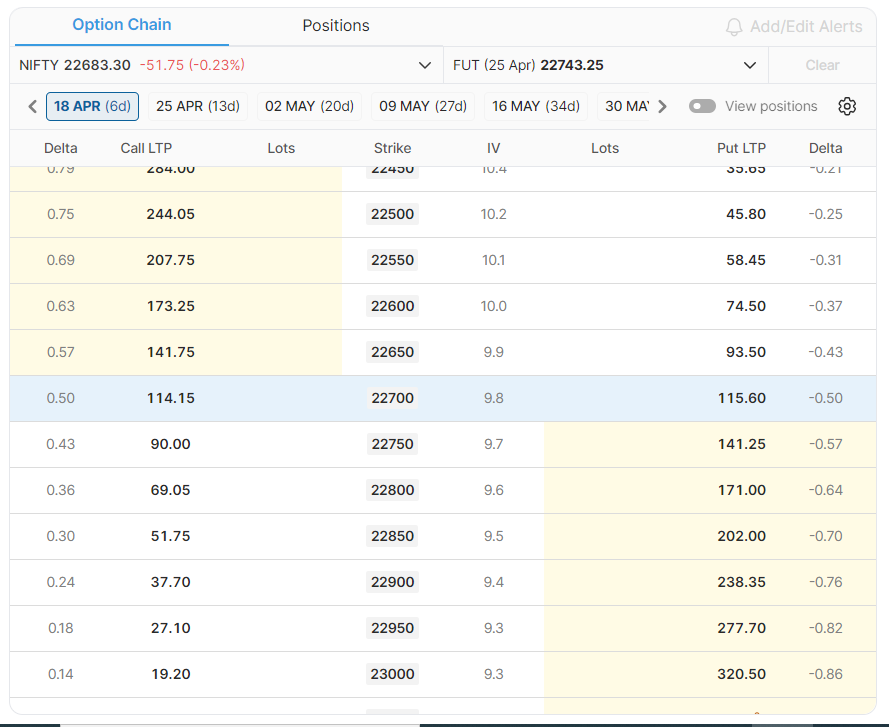

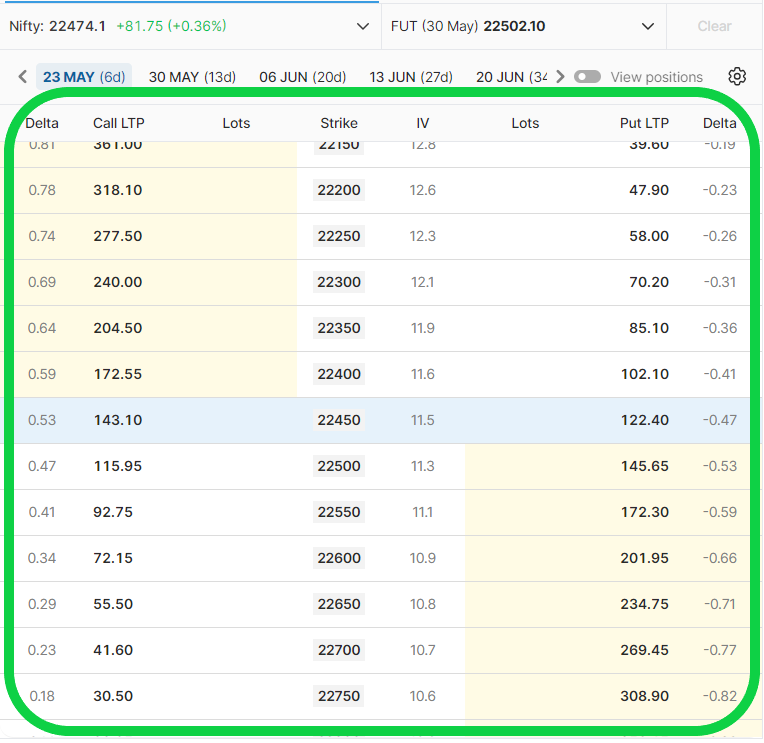

Option Chain may be defined as a list of all option contracts. It covers both calls and puts a certain security. It is also known as an Option Matrix.

Skilled users can utilise the Option Chain to determine the direction of price fluctuations. It also aids in identifying the instances at which a high or low amount of liquidity arises. Typically, it allows traders to assess the depth and liquidity of individual strikes.

It displays all available calls and puts options contracts for a particular underlying security (like a stock or ETF) on an exchange. Each contract represents the right, but not the obligation, to buy or sell the underlying security at a specific price (strike price) by a specific date (expiration date).

The option chain organises this information in a way that's easy to understand. Here are some key elements you'll typically find:

-

Strike Prices: A range of prices at which you can buy or sell the underlying security.

-

Call Contracts: A call is an option contract that grants the owner the right, but not an obligation, to buy underlying securities at a certain price within a given timeframe.

-

Put Contracts: Put options offer the option holder the right, but not the responsibility, to sell an underlying security at a given price within a given timeframe.

-

Expiration Dates: The date by which you must exercise your option to buy or sell. An option's expiration is the specific date and time when the option contract becomes invalid.

-

Option Greeks: The Greeks are letters that represent important measurements of an options contract. They help assess how the price of an options contract may be affected by changes in the underlying security's price (Delta), volatility (Vega), rate of change of the option's delta(Gamma), and time decay (Theta). Understanding the Greeks can help you make better decisions about which options to trade and when to trade them.

-

Bid-Ask Spread: The difference between the highest price a buyer is willing to pay (bid) and the lowest price a seller is willing to accept (ask) for an option contract.

Through a thorough analysis of the option chain, investors can gather valuable insights into the prevailing market sentiment, potential price fluctuations, and the associated costs of various options strategies. This analysis allows traders to make more informed decisions and develop effective trading strategies based on the information gleaned from the option chain.

Overview of AlgoTest Simulator

Have you ever considered the potential of creating a profitable strategy? Would you like to assess the past performance of your strategy? Are you eager to test your discretionary or rule-based strategy using historical option chain data? How about exploring a risk-free environment where you can fine-tune your strategy without financial concerns? Imagine being able to analyse and optimise your strategies according to market conditions without any real money risks!

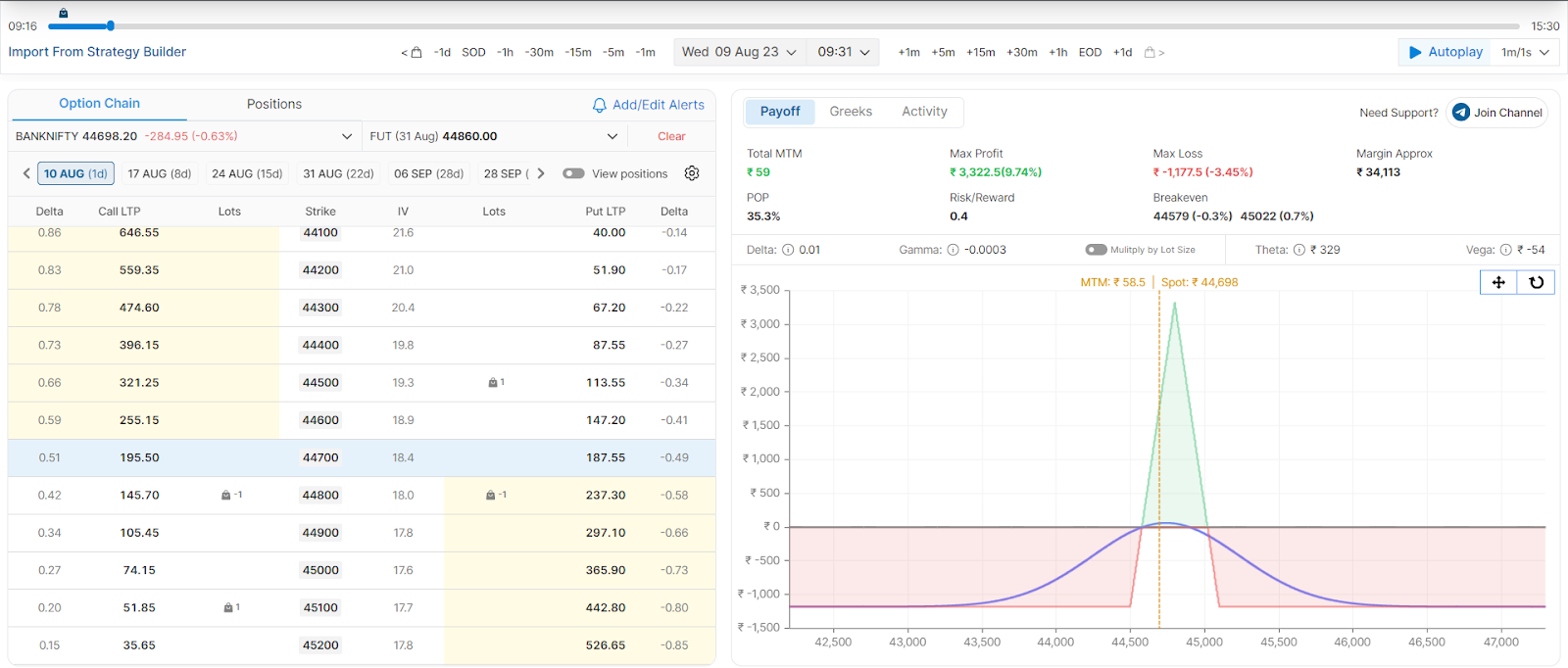

The AlgoTest Simulator is a user-friendly tool designed to help traders analyse and improve their trading strategies using historical market data. It lets users recreate past market conditions, assess their strategies' performance across different periods, and identify strengths and weaknesses before investing real money. The Simulator provides detailed performance indicators, trade insights, and visual representations of data, making it an essential resource for both new and experienced traders looking to make well-informed trading decisions.

Benefits of using AlgoTest Simulator

Here are some key advantages of using AlgoTest Simulator:

-

Backtesting: AlgoTest Simulator allows you to backtest your strategies using historical option chain data, helping you determine their past profitability, associated risks, and rewards. This data-driven approach supports decision-making when trading a particular strategy.

-

Advanced Analytics: AlgoTest Simulator provides advanced analytics for your strategy, including Max Profit, Max Loss, Risk Reward, and Breakeven, helping you fine-tune your strategy based on your risk appetite.

-

Advanced Visualization: AlgoTest Simulator offers a visual representation of your strategy, including a payoff graph, allowing you to assess maximum potential loss and profit based on underlying movements. This advanced visualisation tool assists in making better decisions and optimising your strategy.

-

Strategy Optimization: AlgoTest Simulator helps in optimising your strategy based on market conditions. For instance, if you realise that the risk-reward ratio of your strategy is not favourable in a certain market environment, you can adjust and optimise it accordingly.

-

Scenario Analysis: AlgoTest Simulator assists in analysing different scenarios, allowing you to review past data and identify effective strategies for upcoming events like elections. Additionally, you can analyse strategies using payoff graphs to determine potential gains or losses based on market movements.

-

Increase Confidence: AlgoTest Simulator helps build confidence in your trading strategy by allowing you to backtest and understand its strengths and weaknesses, enabling you to make informed decisions.

-

Increase Profitability: AlgoTest Simulator enables you to fine-tune your strategy to increase profitability by designing strategies suited to different market conditions and optimising them accordingly.