Non-Directional Algo Strategy Sample

These strategies are for demonstration purposes only and are not intended for actual trading. AlgoTest is not responsible for any profit or loss arising from the use of these sample strategies.

Non-Directional Strategy Defined

A non-directional strategy is a trading strategy in which the trader benefits when the market remains within a specific range. The trader can make a profit regardless of whether the market moves up or down within that range. In simple terms, with a non-directional strategy, traders are betting on the market staying sideways. Therefore, if the market doesn't move significantly, the trader makes money. These types of strategies have a higher accuracy of winning as the market often stays sideways.

Meet AlgoTest

AlgoTest is an advanced platform for algorithmic trading. It allows traders to test trading strategies, simulate trades without using real money, and execute strategies accurately. This platform combines market complexity with user-friendly technology.

Pre-built Non - Directional Strategy Template

Are you having trouble creating a non-directional strategy? No need to worry. AlgoTest offers a prebuilt template to help you learn how to create a non-directional strategy and understand what a non-directional strategy looks like.

This sample strategy is provided by AlgoTest so that its users can use it as a guide to create their non-directional strategy.

Access Non-Directional Strategy Template

To get a sample of a non-directional strategy, just follow the straightforward steps outlined below.

- Create an account at https://algotest.in.

- Click on the saved strategy button as shown in the image below

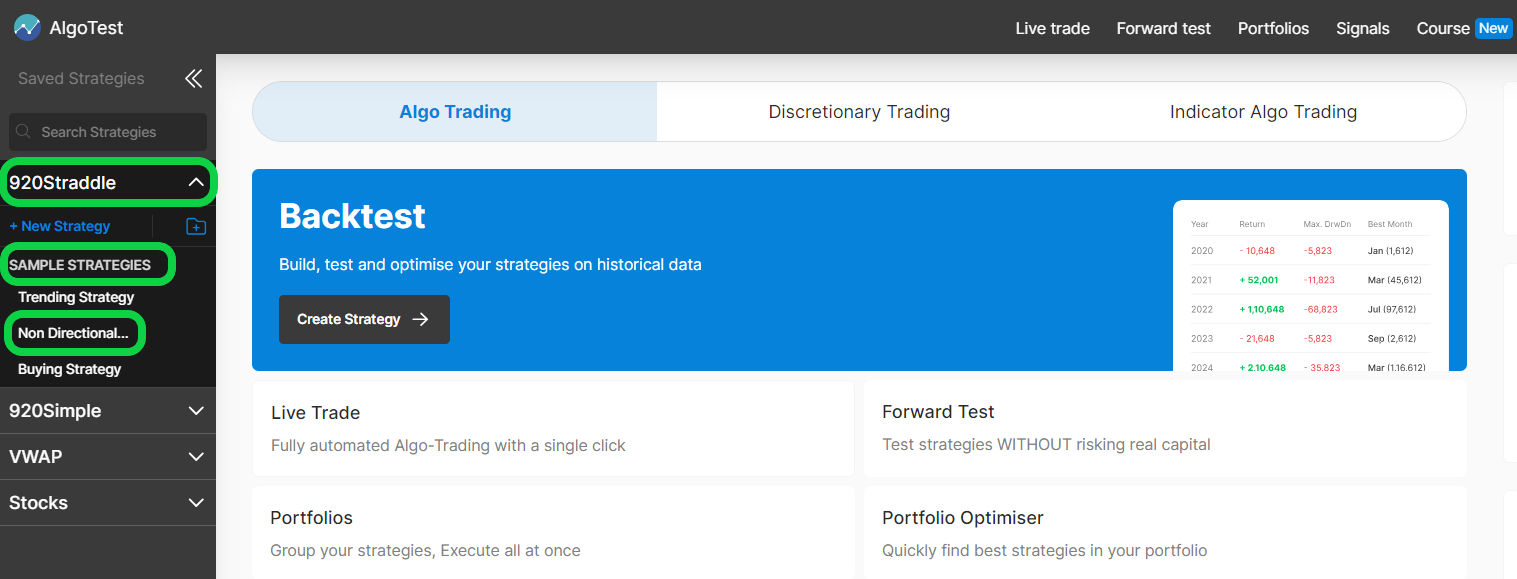

- Click on Non-Directional Strategy under the sample strategy section. It is under the #920 straddle as shown in the image below.

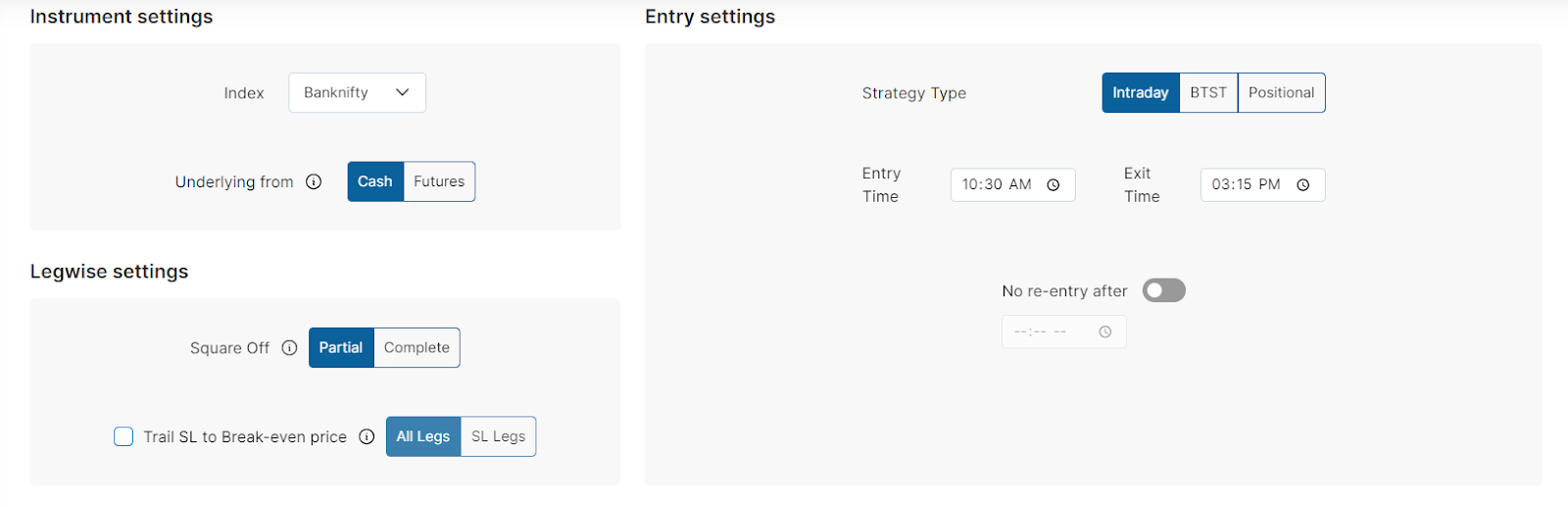

- It will show you a strategy as shown in the image below.

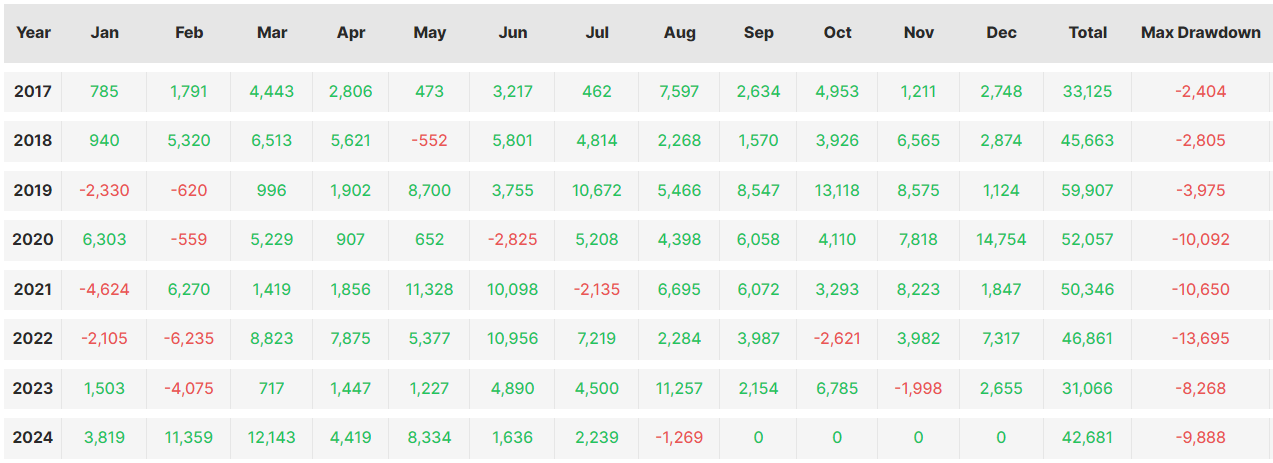

- You can backtest the strategy by clicking on the "start backtest" button as shown in the image below.

The Logic Behind our Non-Directional Strategy

Having a ready-made strategy is just the starting point for a trader. There is no one-size-fits-all strategy in the market, but each strategy comes with its own set of risks and rewards. It's crucial for a trader to fully understand the strengths and weaknesses of their strategy and how it performs under different market conditions.

Considering that the market tends to stay range-bound around 70% of the time, we have the opportunity to develop a strategy tailored to capitalize on this market behaviour. By doing so, we increase the likelihood that the market will move in our favour, enhancing the accuracy of our non-directional strategies.

To take advantage of sideways movement, we will use an option-selling strategy. This means we are betting on non-directional movement by using a wider stop loss on options. A wider stop loss increases the likelihood of staying in the market for longer periods. This is beneficial because options gradually lose value over time (theta decay), even if the market remains at the same price. Ultimately, all at-the-money and out-of-the-money options expire worthless on expiry day.

Strategy Entry & Exit Conditions

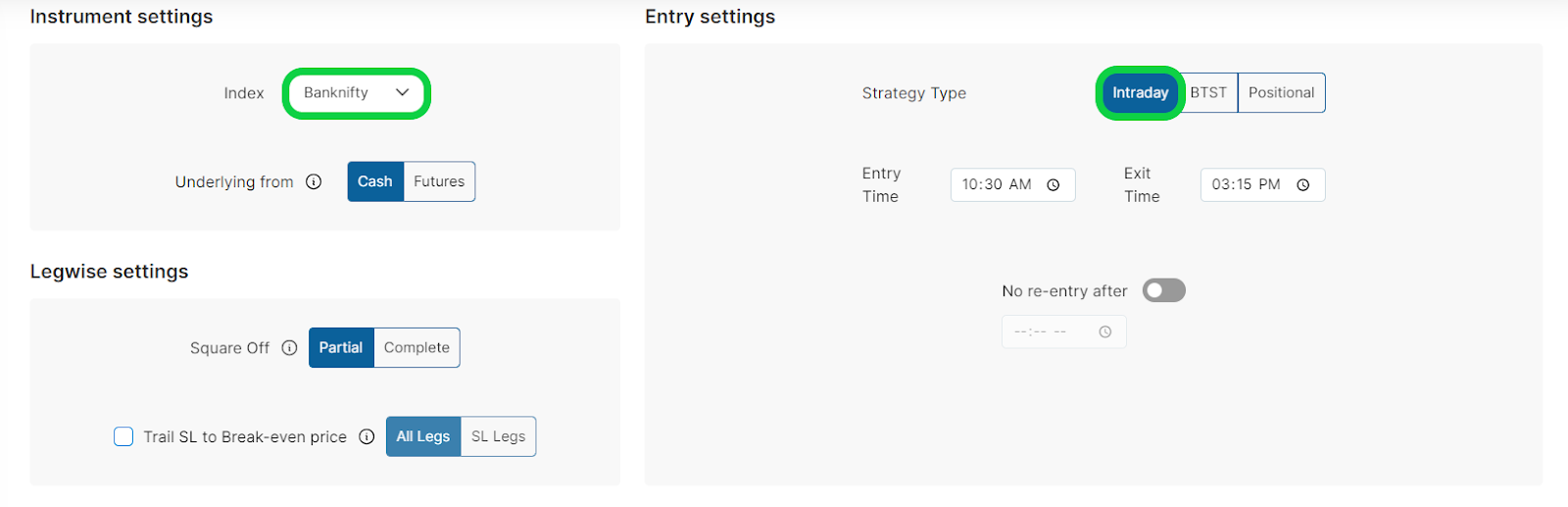

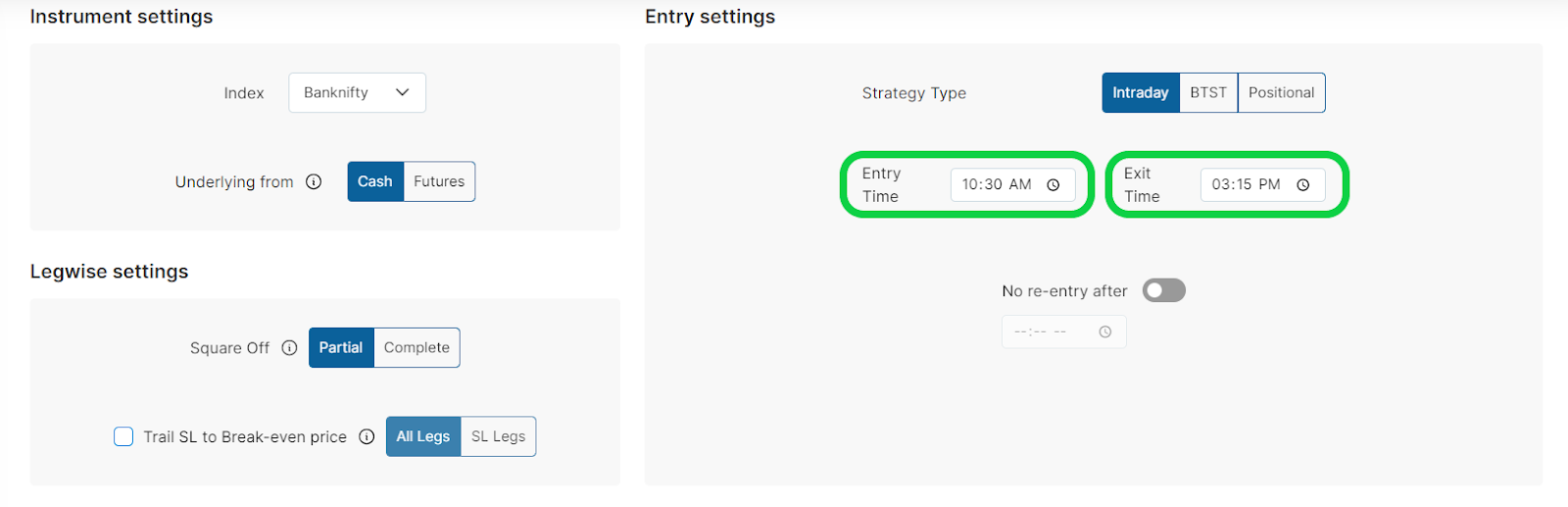

First, we need to determine whether this is an intraday or positional strategy. This will be an intraday strategy to avoid overnight risk, so we will exit the strategy on the same day. Now, we need to select the index on which we want to trade. Although we have selected BankNifty, you may choose any other index. Clearly defined :entry and exit rules are essential in trading.

Entry

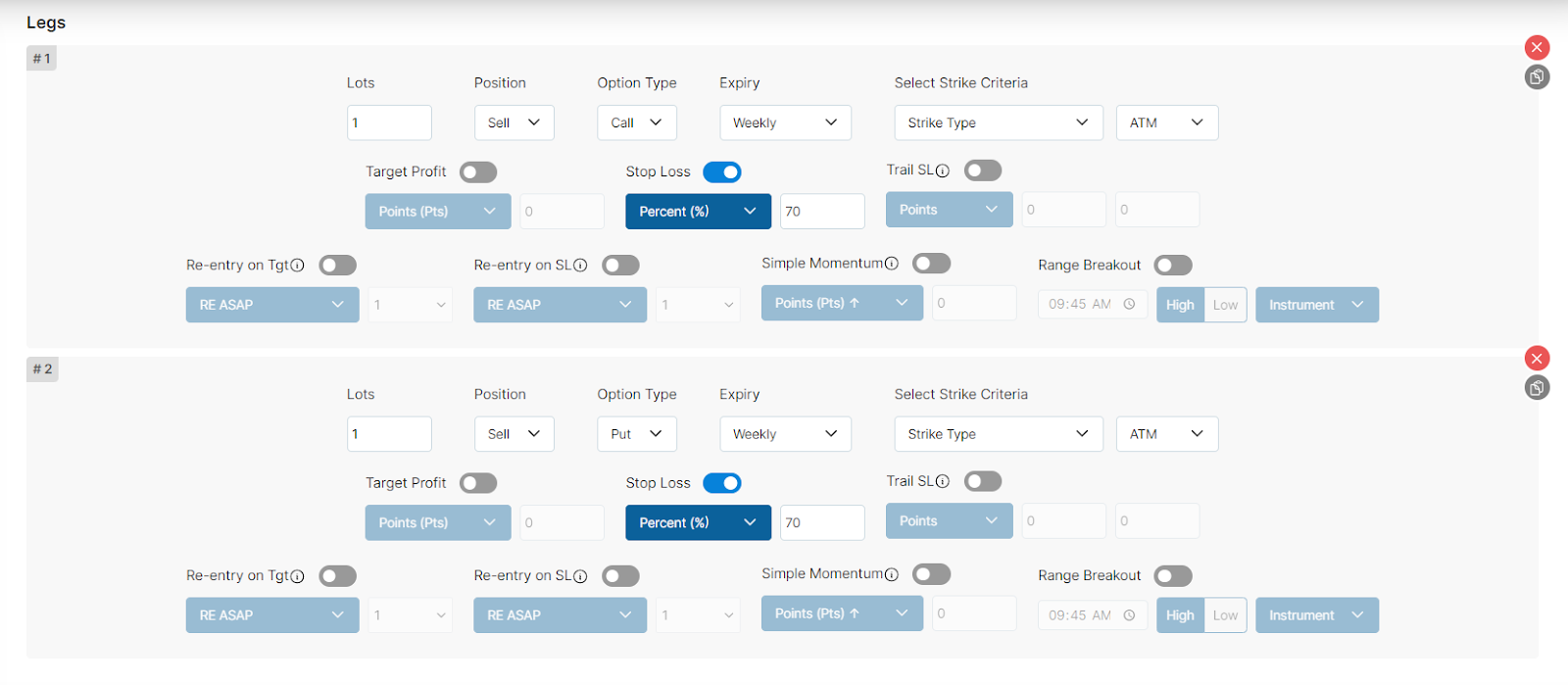

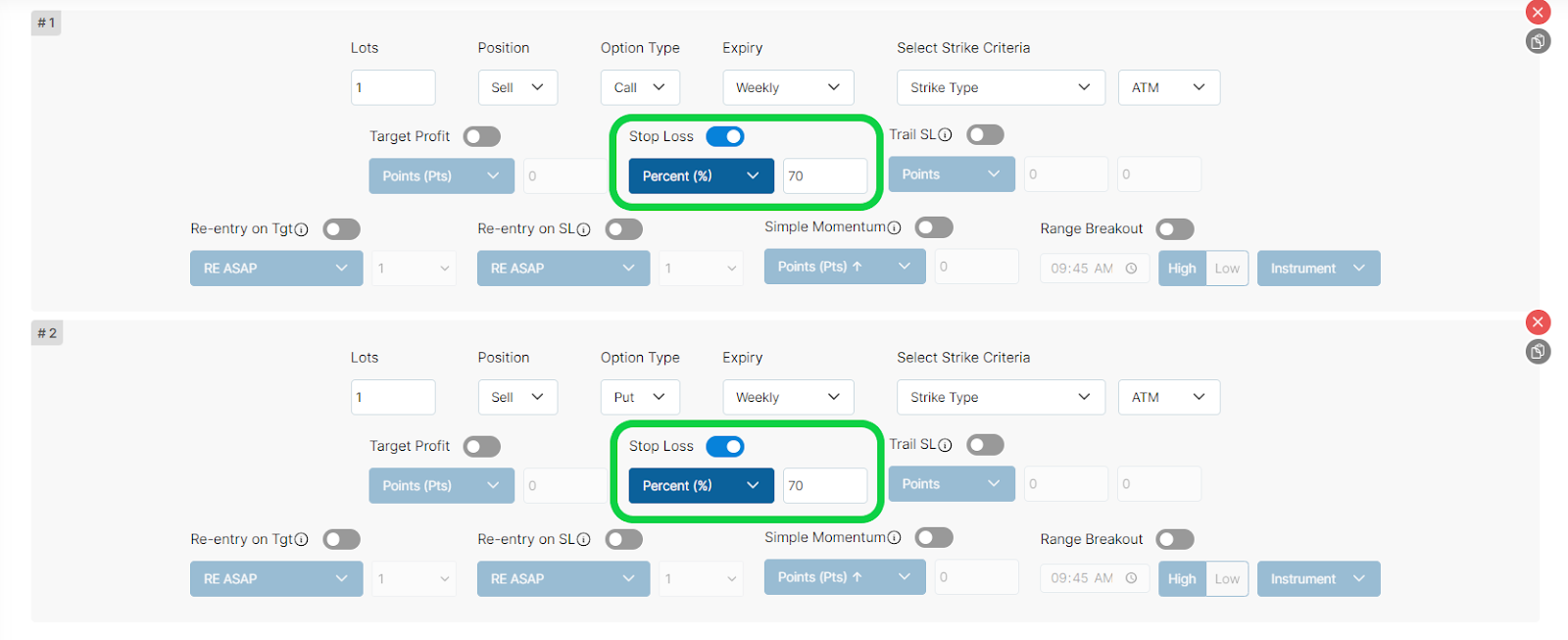

We will sell an ATM Call Option and an ATM Put Option at a specific time of day. To determine the best time to do so, you can backtest your strategy at different times using AlgoTest. Market movement is typically high in the morning, which is not ideal for a non-directional strategy. Therefore, we have selected 10:30 AM as the entry time for our sample strategy. Based on this, we will sell the ATM Call and ATM Put at 10:30 AM. As this is an intraday strategy, we will also exit our positions at 03:15 on the same day.

We can add an ATM CE & ATM PE Leg from the leg builder by clicking on the Add Leg button.

Exit

However, having good accuracy in a non-directional strategy doesn't always guarantee that the market will move in our favour. There will be days when the market doesn't go our way, or when it's in a trending phase, which is a nightmare for a non-directional trader. To manage risk, we will set a stop loss of 70% on each Call Option (CE) and Put Option (PE) leg. So if the market moves in one direction and hits our stop loss on one side, the other side will end up giving some profit.

Advance Risk Management

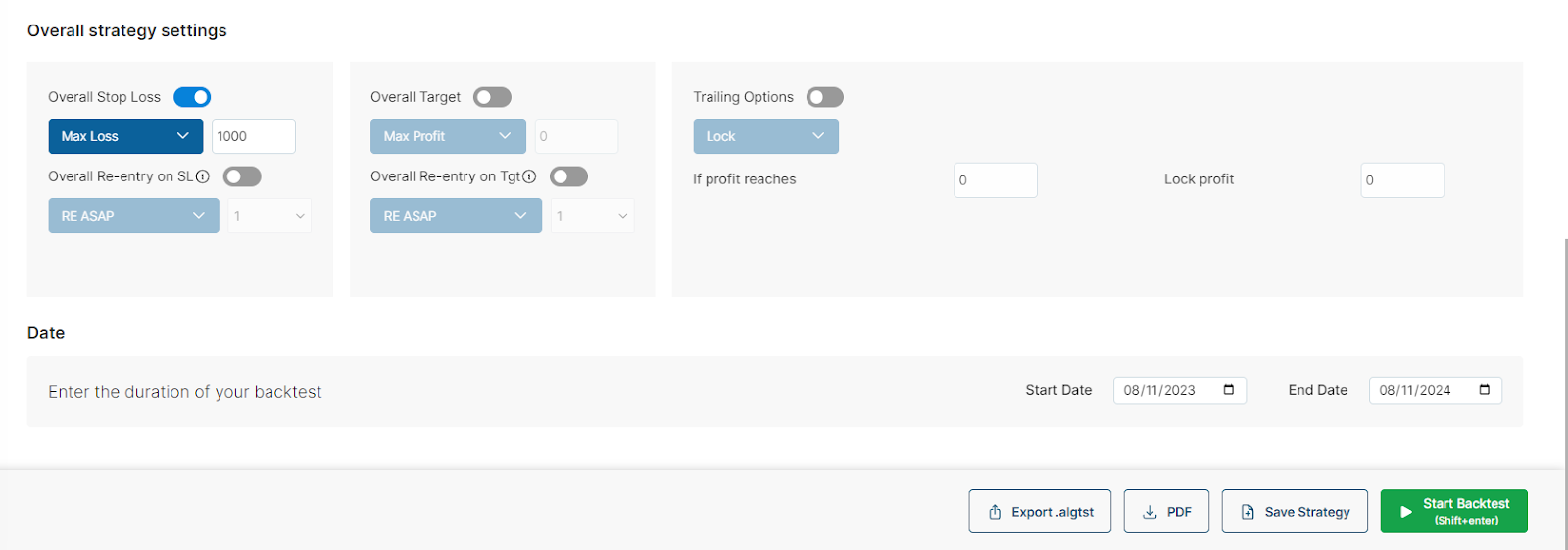

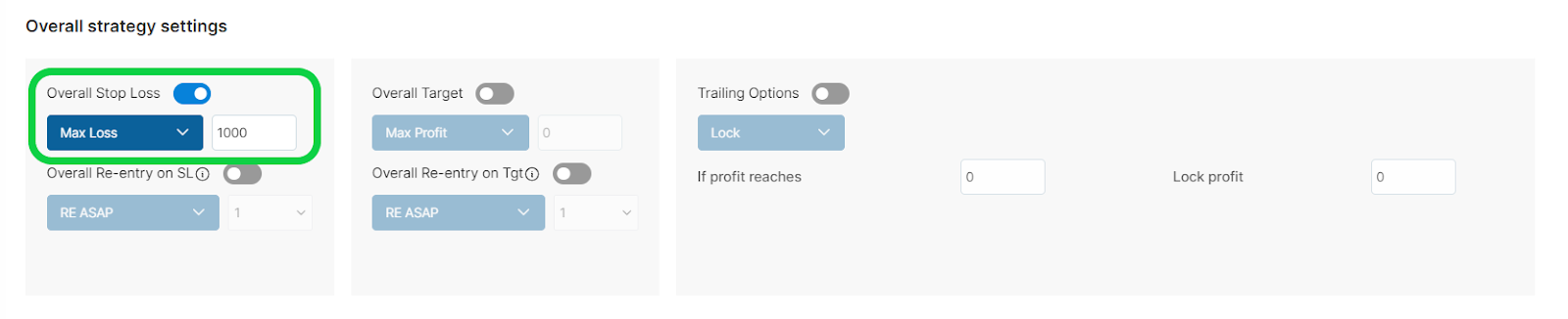

A trader must have a strong psychology. A significant loss in a single trade can disrupt your ability to trade systematically. To mitigate this risk, we will limit our daily loss for the strategy to Rs. 1000 per lot. This limit will be applied to the combined strategy, meaning that if our strategy incurs a loss at any point in the day, we will cease trading for that day.

Conclusion

There is no holy grail in the stock market. Every strategy we create has its pros and cons. No single strategy can guarantee profits every day. Therefore, it is always better to use the sample strategies provided by AlgoTest to get an idea and create your strategy based on your risk tolerance. You can try different permutations and combinations and backtest your strategy using AlgoTest to understand how it will perform in different market scenarios.