Portfolio Backtest

The AlgoTest Portfolio feature enables you to backtest multiple strategies simultaneously with just one click. It will display the combined backtest results and statistics of multiple strategies. You can backtest up to 50 strategies together in 1 portfolio.

This feature is very useful for traders who want to diversify their capital across multiple strategies. Traders will be able to view the backtest results of a diversified portfolio to understand how running multiple strategies together can improve their overall results.

How to Use AlgoTest's Portfolio Feature

You can easily use the AlgoTest Portfolio feature by following these simple steps:

-

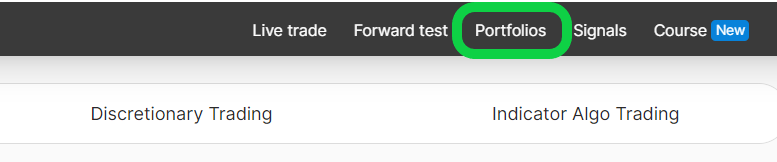

Visit the AlgoTest website and click on the "Portfolios" button, as shown in the image below.

-

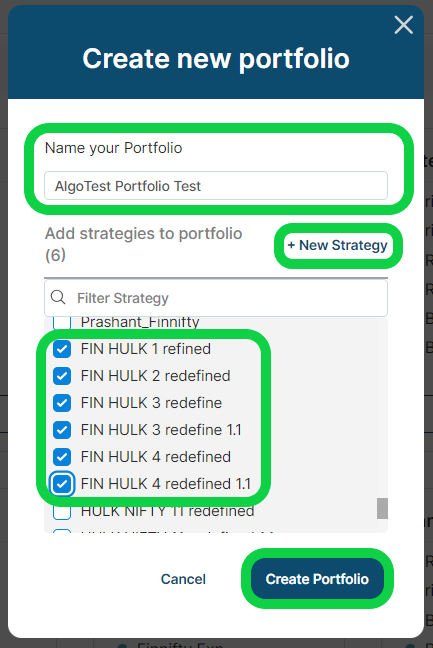

Click on the "Create New Portfolio" button as depicted in the image below.

- Now select the strategies you want to backtest together, give a desired name to your portfolio, and click on "Create Portfolio." You can also create a new strategy by clicking on the "Create New Strategy" button.

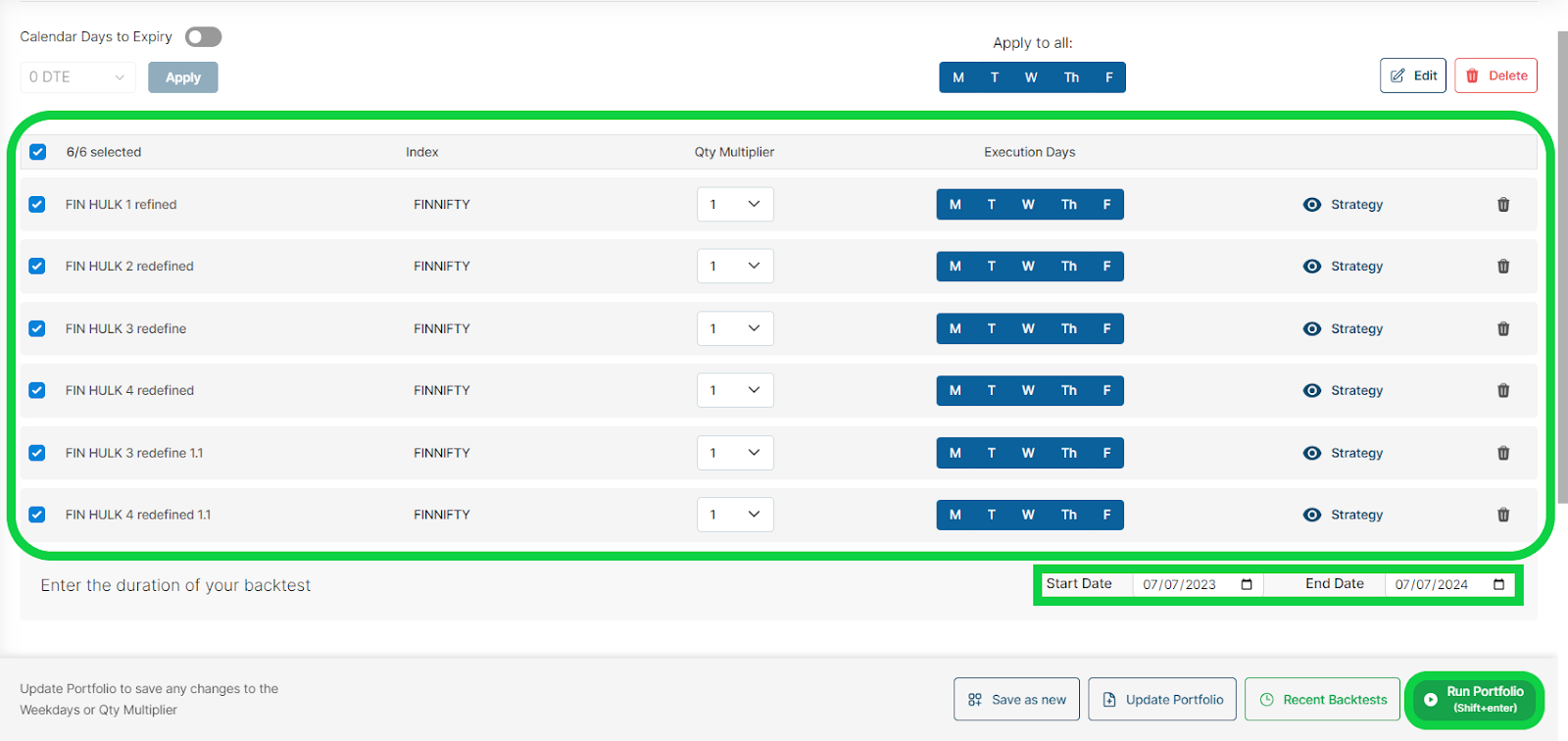

- Now you can view the strategies in your portfolio. You can choose the time period for backtesting and then run the portfolio by clicking on the "Run Portfolio" button.

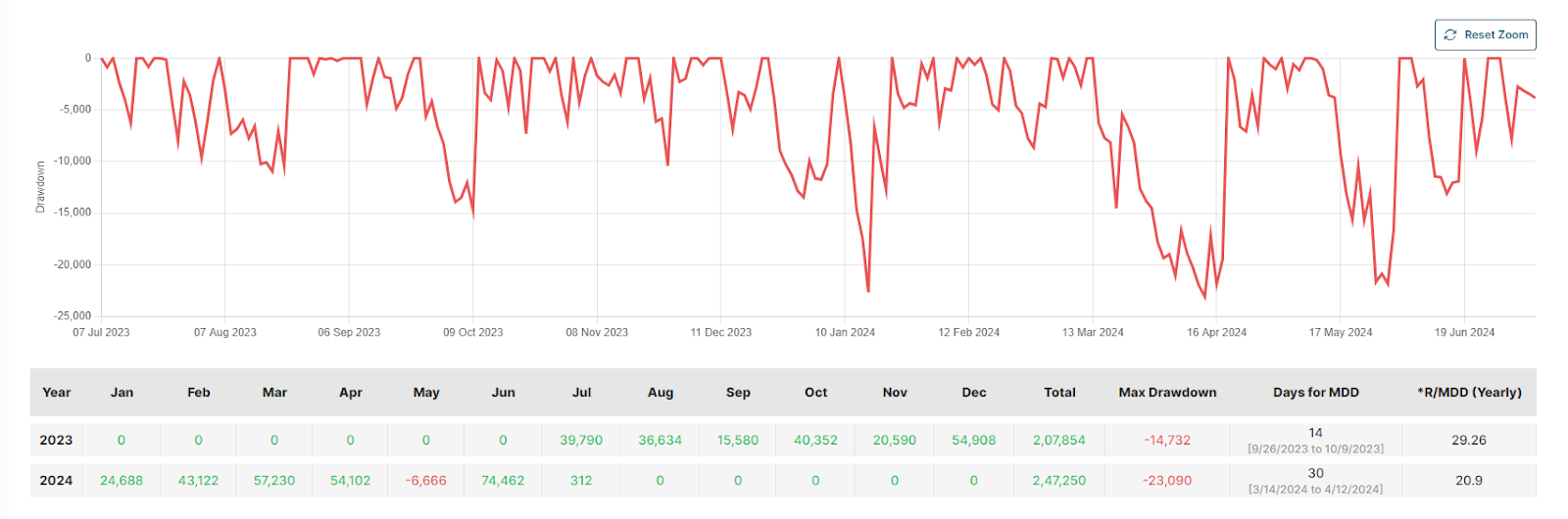

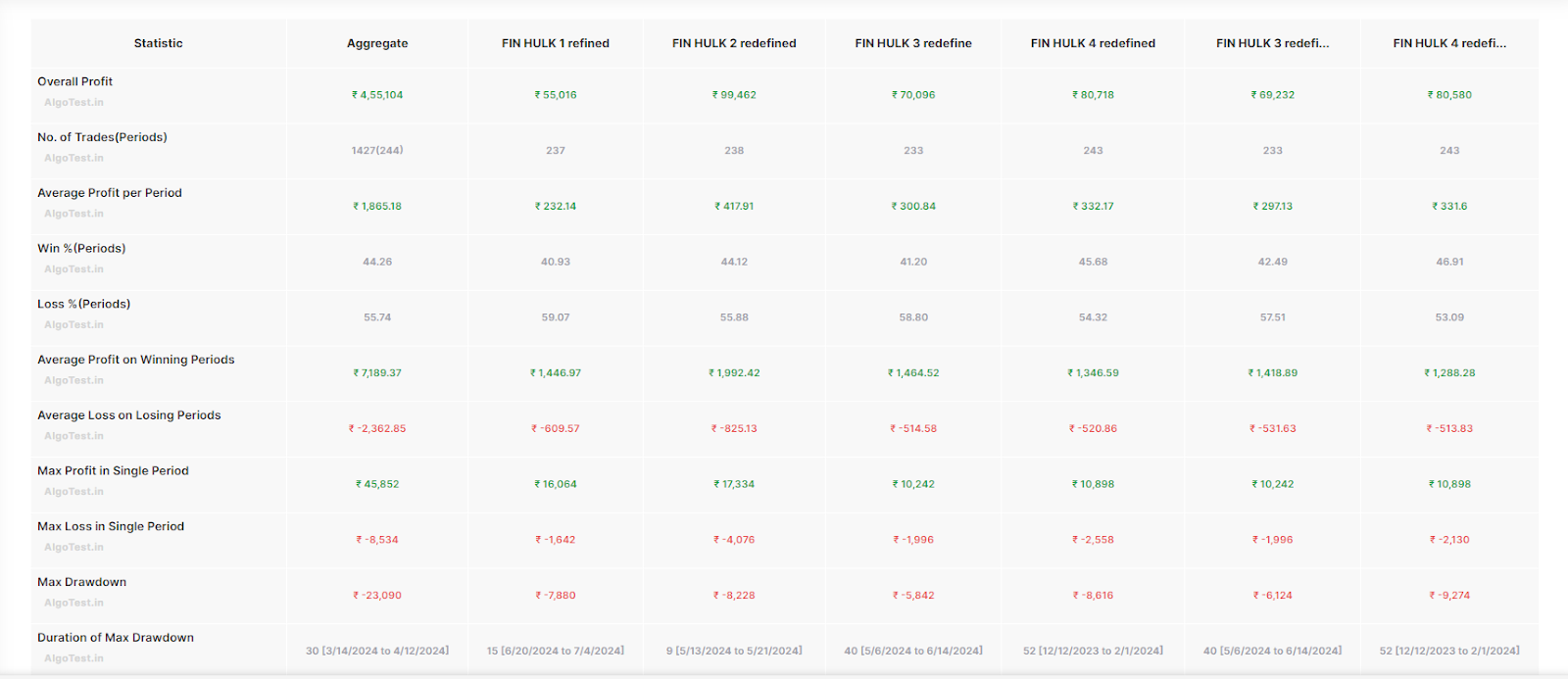

- You can view the combined backtest result of strategies in the image below.

As shown in the image above, the portfolio backtest displays the backtest results of multiple strategies together and on an individual basis.

Advanced Features

There are advanced features available in portfolio backtesting that can enhance your results and improve your portfolio.

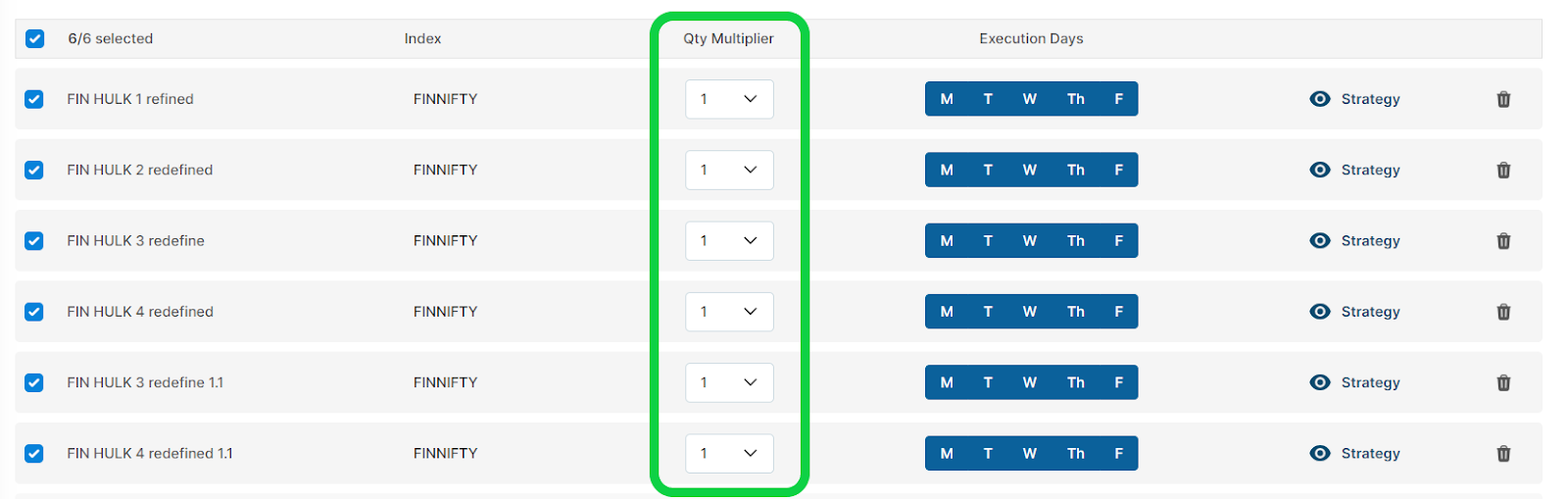

Quantity Multiplier

This feature enables the multiplication of quantities in individual strategies within a portfolio and allows for filtering of backtest results based on strategies with different quantities.

- Click on the Quantity Multiplier button, which is shown in the image below.

- You can select the quantity from the drop-down menu, as shown in the image below.

Day Filter

You can use this feature to filter your portfolio backtest results based on the chosen days for strategies, enabling you to optimize your strategy on a daily basis.

- You can utilize this feature by selecting specific days, as demonstrated in the image below. It will refine the backtest results according to the days you have chosen.

DTE Filter

Our convenient DTE filter allows you to tailor your approach based on the days remaining until expiry. This feature is designed to optimize and fine-tune your portfolio according to the specific distance from the expiry day of the instrument.

What is DTE?

DTE stands for "days to expiry." In simple terms, you can adjust your strategy based on the number of trading days remaining until the contract expires.

Trading days to Expiry means:

It only includes trading days and doesn't include weekends and market holidays.

For example:

If the Sensex expiry is on Tuesday then Monday will be DTE -1 and Friday will be DTE-2.

If you want to backtest the portfolio only on the day of expiry, the distance from expiry is 0 days. This is commonly referred to as "0 DTE." This approach will display the results specifically for the day of expiry for the particular contract.

Let’s take an example of Sensex weekly expiry and assume Tuesday (14th Jan 2025) is the expiry. How are the days selected based on the distance from the expiry in the portfolio backtest in the DTE Filter?

| DTE | No. of Days from Expiry | Date |

|---|---|---|

| Day to Expiry = 0 | Expiry day, i.e., Tuesday | 14th Jan, 2025 |

| Day to Expiry = 1 | 1 day before expiry, i.e., Monday | 13th Jan, 2025 |

| Day to Expiry = 2 | 2 days before expiry, i.e., Friday | 11th Jan, 2025 |

| Day to Expiry = 3 | 3 days before expiry i.e., Thursday | 10th Jan, 2025 |

| Day to Expiry = 4 | 4 days before expiry i.e., Wednesday | 09th Jan, 2025 |

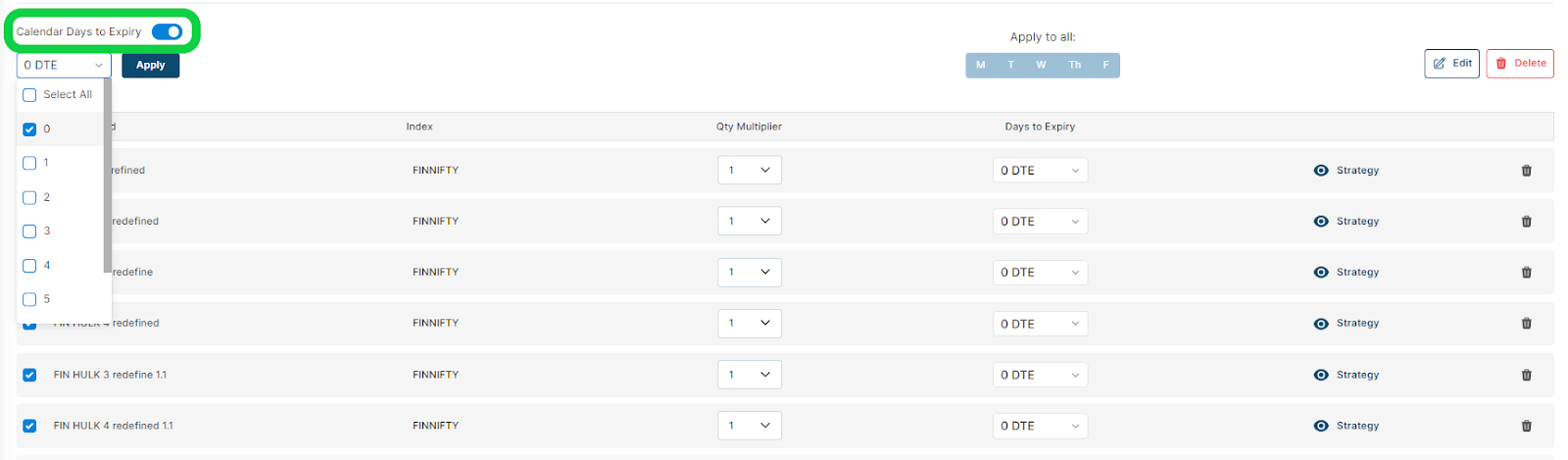

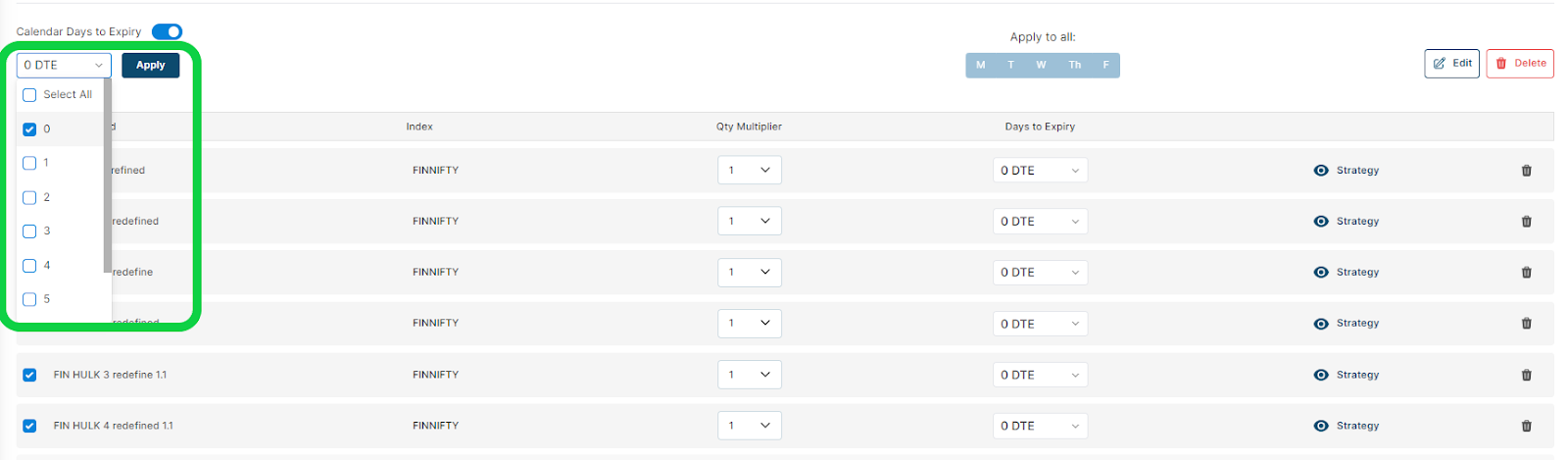

You can enable the DTE filter as shown in the image below.

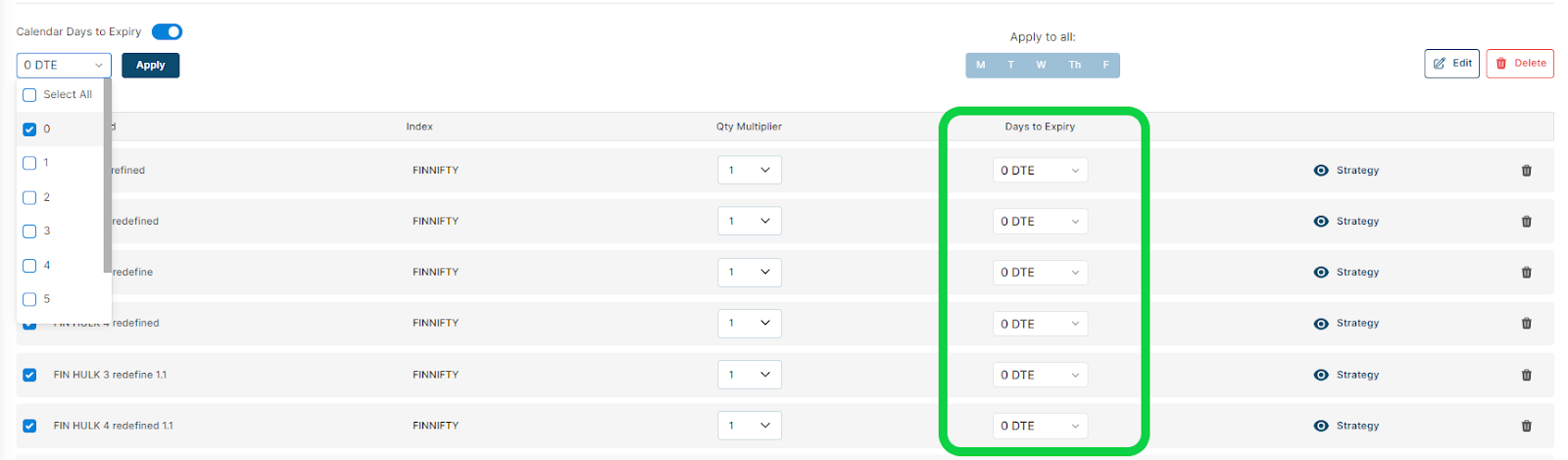

- Now select the days from the options given in the dropdown menu as shown in the image below. Then, click on the apply button to apply to all the strategies.

- You can also choose to apply the DTE filter individually to the strategy, as shown in the image below.

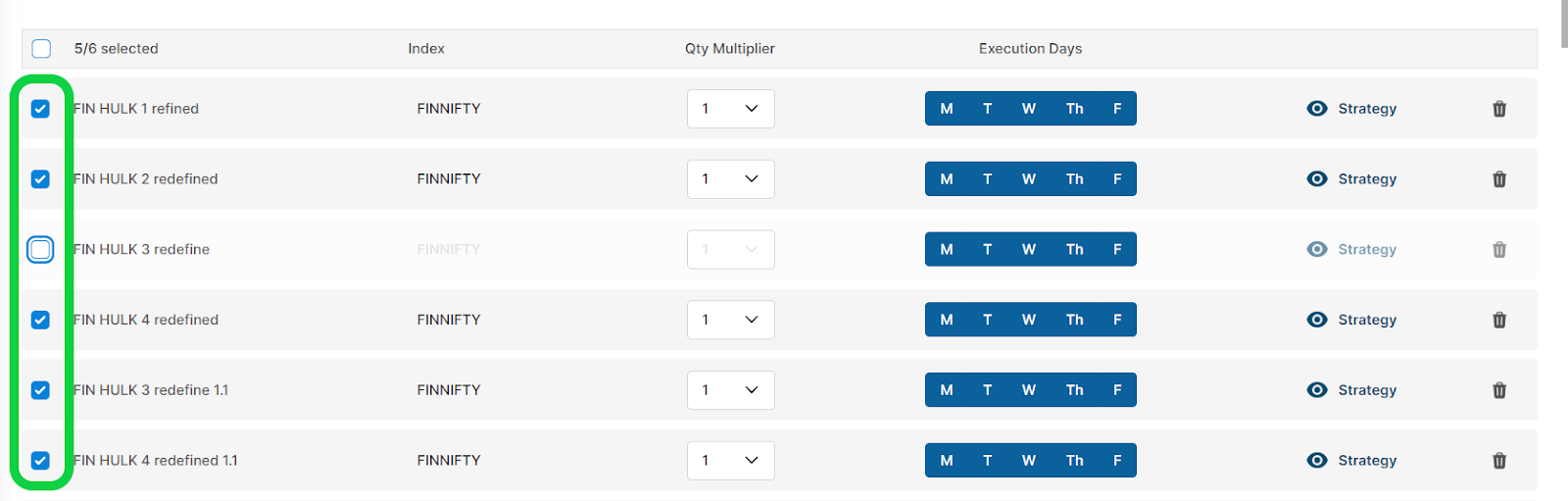

Enable/Disable Strategy

This feature allows you to filter out your backtest results based on your chosen strategy. For example, if you backtest a portfolio of 30 strategies and want to remove some of them from the backtest results, you can simply deselect those strategies, and the backtest results will be filtered accordingly.

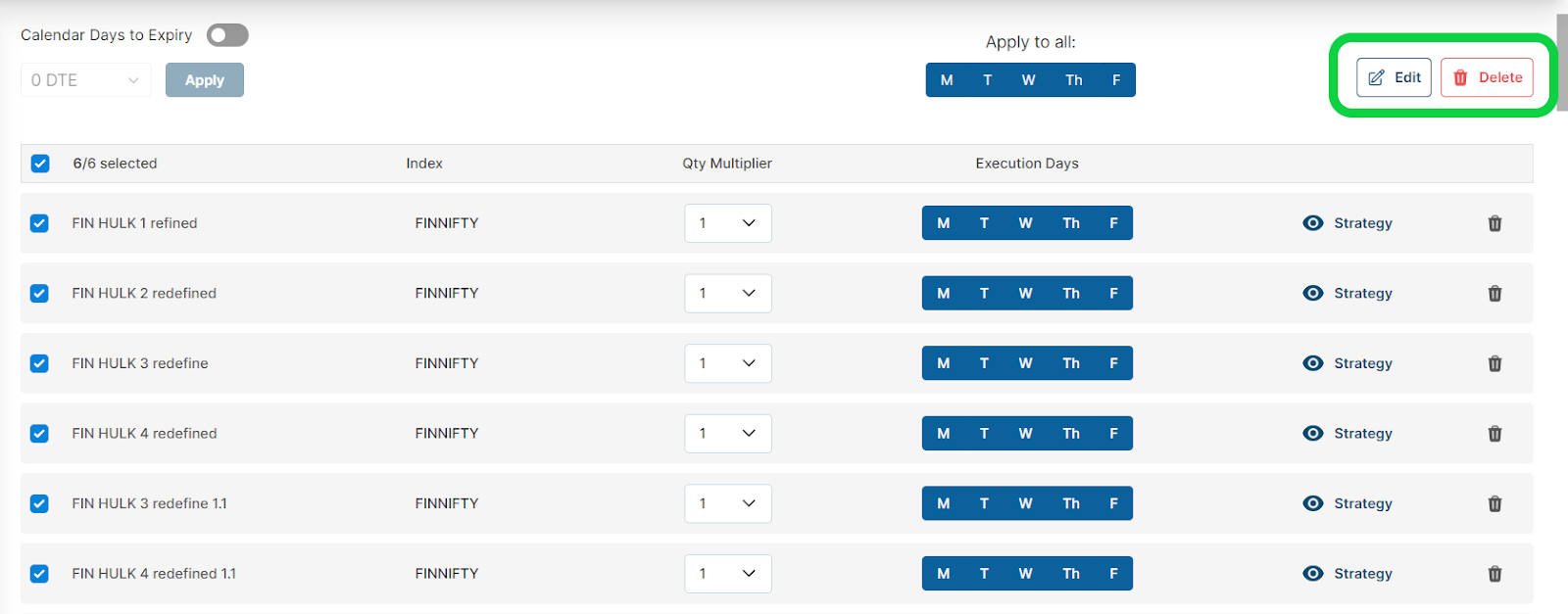

Edit/Delete Portfolio

This feature allows you to edit or delete your portfolio. You can click the edit button to edit your portfolio and add or remove a strategy from it. You can click the delete button to remove the portfolio.